Is 20% down the best option? While we all navigate this interesting, ever changing market I have recently been having a lot of conversations around affordability, down payment norms, and what is the best percentage to put as your down payment.

While markets shift, so do the options and products loan originators / mortgage brokers offer to the consumer. Of course, the larger the down payment, the smaller your loan. Traditionally, smaller the monthly payments result from the above, yet today we are in the territory of seller credits, temporary and permanent interest rate buy downs, I am frequently seeing sellers pay some additional funds to the buyers closing costs or buy downs allowing the buyer to lock in a lower interest rate. Resulting in the monthly payment being lower with less money down.

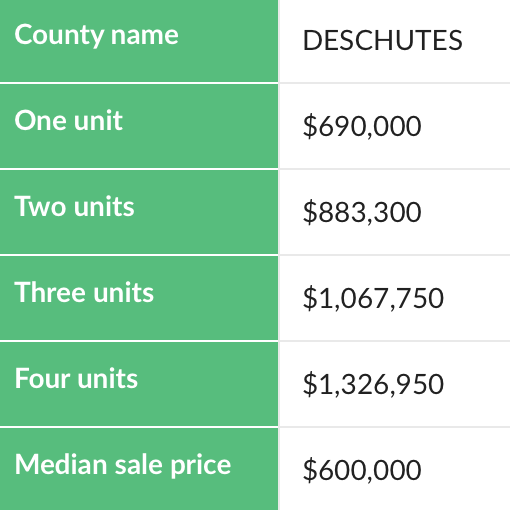

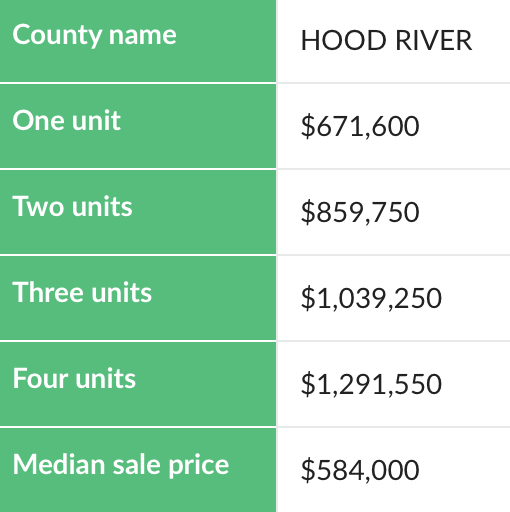

So hypothetically let's say you are buying a duplex or a single family that you are going to live in, you explore the conventional loan and the FHA loan options. Because there are fewer bidding wars and fewer multiple offers, you can get away with very little down, 3% of the purchase price down if you decide to go the FHA route. Again, FHA does not mean "First Time Homebuyer Loan" it was a product created during the 1930 recession to keep the economy going, it stands for Federal Housing Administration. There are a few perimeters with an FHA loan, the loan limits are in correlation with the county median home price, so if you're buying in Deschutes County or Hood River County (two of the most expensive in Oregon) the loan limits are higher than if you were shopping in any other county.

A brief summary of the FHA requirements:

1. The percentage one puts down is in correlation with your credit score, if your credit is between 500 and 579, you may still qualify for an FHA loan, but a 10% down payment is required. 3.5% is required if your credit score is at least a 580.

2. The condition of the home must pass FHA appraisal requirements. The roof cannot be past it's life, the exterior paint must be in okay condition etc.

3. You, the borrower, must have a Debt to income ratio of 43% or less.

4. Mortgage insurance is required.

5. Lastly, the structure whether it's a single family or multi family must be your primary home.

This is interesting as a seller too, if you're in the process of listing your home and want the largest audience of buyers, make sure it passes the FHA requirements above.

Click this

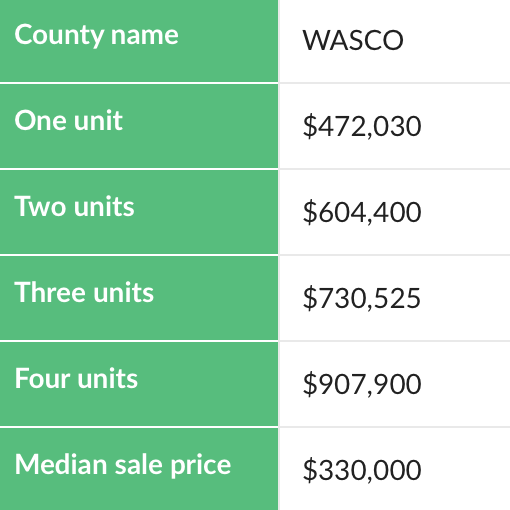

link to view all FHA county limits in Oregon. Below are three counties I work in.